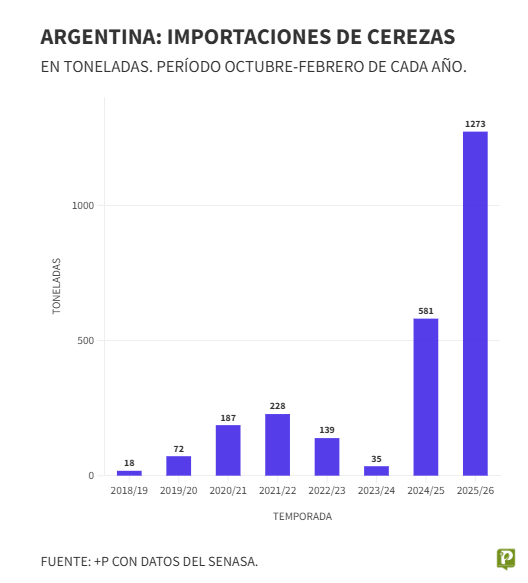

Cherry imports reached 1,273 tonnes in the 2025/2026 season, the highest volume ever recorded in the Argentine market.

The 2025/2026 cherry season will go down in history as a true turning point for the Argentine market. Not only because of the challenging international context or the climatic difficulties affecting local production, but above all due to a figure that marks a before and after: between October 2025 and February 2026, imports totaled 1,273 tonnes, an all-time record for Argentina.

This figure, which could still increase slightly once March data are consolidated, implies a year-on-year growth of 120% and an increase of over 360% compared to the average of the past five years. Statistically, the shift is clear. Structurally, it raises deep questions about the future of the sector.

There is another element that amplifies the scale of the phenomenon: 100% of the imported volume comes from a single country, Chile. Understanding what is happening in the Argentine market necessarily requires understanding the transformation—and the overproduction crisis—currently affecting the leading exporter in the Southern Hemisphere.

The context: Chile’s structural expansion

The season began last October in a scenario that already hinted at tensions. Chile was consolidating an aggressive expansion strategy in cherry cultivation. New plantings, the introduction of high-yield genetics, improvements in logistics and post-harvest technologies supported a steady increase in production.

The result was a record harvest that encountered unexpected limits in destination markets, as had already happened in the previous season. Over the past decade, Chile’s growth has been strongly driven by Asian demand, particularly from China, where cherries have positioned themselves as a premium product associated with celebrations and gifts. However, in this season, signs of saturation have re-emerged: higher stocks, increasing competition and logistical pressures that have impacted prices.

Not even Europe and the United States

Neither Europe nor the United States showed the capacity to absorb such significant increases in supply. The result was a decline in prices in the main destination markets and an urgent need to diversify commercial outlets. In this reconfiguration, Latin America gained central importance, and Argentina emerged as one of the key markets to test. Shipments from Chile to Argentina increased by more than 100% in just one year. This explains the record of 1,273 tonnes imported in the current season.

The Argentine cherry market has a distinctive feature: it is a niche market. Unlike other mass-consumption fruits, cherries are concentrated in high-income segments, with greater penetration in large urban centers and a strong presence in specific periods of the year.

With prices exceeding 10 dollars per kilo (around €9.20/kg) in the wholesale channel, the Argentine market managed to maintain values despite the record level of imports.

With prices exceeding 10 dollars per kilo (around €9.20/kg) in the wholesale channel, the Argentine market managed to maintain values despite the record level of imports.

In this context, the arrival of over one thousand additional tonnes initially seemed like a direct threat to price stability. Economic logic would suggest that such a sharp expansion in supply in a relatively small market should have pushed prices downward. However, the collapse did not occur. And to understand why, it is necessary to consider another key factor of this season: increased demand.

The impact of hail in Patagonia

Argentine production, concentrated in the Patagonian region, went through a climatically complex season. Heavy rains and hailstorms affected large areas of northern Patagonia, particularly in the provinces of Río Negro and Neuquén.

The damage not only reduced volumes but also compromised the quality of part of the crop. A significant share of production originally destined for export was redirected to the domestic market, failing to meet the standards required by foreign buyers.

A particular phenomenon emerged: the domestic market simultaneously received more local product—non-exportable—and the record volume from Chile. In theory, a double increase in supply. Yet, price trends showed remarkable resilience.

Statistics from the Mercado Central de Buenos Aires (MCBA), where about 30% of the country’s cherries are traded, allow this dynamic to be observed with precision.

Between October, November and December 2025, wholesale and retail prices were above the levels recorded in the same period of the 2024/2025 season. In several weeks of the last quarter of the year, prices exceeded 10 dollars per kilo in the wholesale segment (around €9.20), equivalent to approximately 14,000 pesos per kilo at the reference exchange rate.

Between January and February, values stabilized compared to the previous season, within a range of 5 to 7 dollars per kilo (around €4.60–€6.40). However, on average, prices in dollars were slightly higher than in the previous cycle. The data is significant: the market absorbed higher volumes without compromising producer profitability.

The logic of the ABC1 segment

The explanation lies, in part, in the nature of cherry consumers in Argentina. They mostly belong to the ABC1 segment, with high purchasing power and low sensitivity to price changes when quality meets expectations.

The growth of Chilean cherry imports reflects the structural expansion of the trans-Andean export sector and its impact in Latin America, where Argentina is consolidating as a strategic destination.

The growth of Chilean cherry imports reflects the structural expansion of the trans-Andean export sector and its impact in Latin America, where Argentina is consolidating as a strategic destination.

Cherries are perceived as a premium product, associated with freshness, distinctive taste and strong seasonality. When the fruit maintains firmness, size and presentation, consumers accept high prices. In this season, both imported and local fruit maintained acceptable standards at retail. This consistency helped sustain product positioning and avoid destructive price competition.

Moreover, greater product availability increased visibility at retail level and stimulated moderate demand growth within the same socioeconomic segment. This was not mass consumption, but rather an expansion within a niche market that reacted positively.

A fragile balance for the future

Although the 2025/2026 season can be considered balanced in terms of prices and profitability, the future scenario raises concerns. Chile forecasts exports close to 135 million boxes for the next season, equivalent to over 650,000 tonnes. The comparison with Argentina is telling: in an optimal year, the country may reach around 8,000 exportable tonnes.

The scale gap is enormous. For Chile, redirecting a small percentage of production to Argentina is a marginal move. For the Argentine market, the same volume can deeply alter internal balance. If Chile’s structural overproduction consolidates and traditional markets continue to show absorption limits, Latin America—and Argentina in particular—could receive even larger flows in the coming seasons. This is where the main concern of the local sector lies.

Paradoxically, the difference in scale may also work in Argentina’s favor. The country does not compete on volume, but can compete on quality and segmentation. Argentine cherries, produced under the unique agroclimatic conditions of Patagonia, are recognized for their firmness and organoleptic characteristics. Smaller scale allows greater commercial flexibility: placing small volumes in specific niches, providing personalized customer attention and building high value-added relationships.

While Chile requires large markets to absorb its massive production, Argentina can target selective destinations where competition is less intense and prices more attractive. The strategic key will be to strengthen this differentiation and avoid direct price-based competition.

The next season under scrutiny

With most of Argentina’s production already marketed and no expectation of major movements in March, attention shifts to the next season. If Chile effectively increases its supply to the projected levels, the regional market may face new tensions. Argentina will have to decide whether to strengthen its presence in the domestic market—which this year proved resilient—or intensify efforts to open new export outlets.

More product, more supply and an unexpected record: Argentina imported 120% more Chilean cherries in just one year. The market absorbed the impact, but the next cycle will be decisive.

Recent experience offers a clear lesson: the record level of imports did not trigger the collapse many feared. The combination of adverse climatic conditions, which limited exportable local supply, consistent retail quality and active premium demand helped sustain prices. However, this balance may not automatically repeat if conditions change.

The 1,273 tonnes imported between October and February represent much more than a simple figure. They are a signal that the Argentine market is now an integral part of the regional cherry strategy. The 120% annual growth and the 360% increase compared to the five-year average show how quickly flows can intensify when the international context allows it.

The real question is whether this phenomenon will be remembered as an exceptional episode linked to a record Chilean harvest or as the beginning of a new phase of deeper regional integration and structural competition.

For now, the 2025/2026 season leaves a distinctive balance: record imports, sustained prices, preserved profitability and a clear signal for the future. In a sector where global scale is concentrated in a few players and where logistics and quality determine success, Argentina will need to rely on its main competitive lever: differentiation.

The record is now part of the statistics. What happens in the coming seasons will determine whether this was a temporary anomaly or the beginning of a structural transformation of the Argentine cherry market.

Javier Lojo

Mas Produccion

Opening image source: Stefano Lugli

Cherry Times - All rights reserved