Germany is the third-largest importer of fresh cherries worldwide, after China/Hong Kong and Russia. From 2010 to 2022, between 52% and 77% of the cherries consumed in Germany were imported, with most imports coming from other EU member states. The largest non-EU suppliers of cherries are Turkey for sweet cherries and Serbia for sour cherries.

German cherry production for MY1 2024/25 is estimated at 41,085 MT. This represents a 2.3% increase compared to the very low production of the previous year, but 13% below the ten-year average (2014-2023). The low production is largely due to unfavorable climatic conditions (late frosts and excessive rain) during pollination.

Furthermore, the actual harvested production could be significantly lower due to thunderstorms with heavy rain and hail that occurred after production estimates were made in July. Opportunities for fresh U.S. sweet cherries are better in August/September, after the German domestic growing season. The processing of cherries into dried fruit is uncommon in Germany. The low demand for dried cherries is met through imports.

I. Area

The harvested area for sweet and sour cherries is expected to amount to approximately 5,684 hectares and 1,533 hectares, respectively. Germany is more competitive in the sweet cherry sector than in the sour cherry sector. Most of the sweet cherry production is destined for fresh consumption, and consumers are willing to pay a premium for locally produced cherries. In contrast, most sour cherries are destined for processing.

When farmers plant new sweet cherry orchards, the trend is toward protected production. This solution requires a higher investment but offers protection against rain and allows the farmer to use predators as a pest management tool.

According to a newspaper article2, the investment costs significantly exceed 100,000 euros per hectare (around $344,100 per acre). The most demanded varieties are Bellise, Burlat, Kordia, and Regina for sweet cherries, and Schattenmorelle and Morellenfeuer for sour cherries.

The results of the latest German fruit tree census of 20224 showed that the area planted with cherries has decreased by nine percent compared to 2017. However, the decline in sour cherries (down 20 percent) was much more pronounced than the decline in sweet cherries (down 5.4 percent).

This is due to strong competition from other EU member states. According to German industry sources, other EU member states, such as Hungary and Poland, have lower production costs and are more competitive in sour cherry production than German producers.

II. Production

Based on harvest assessments made on June 10, the German Federal Statistical Office (destatis) estimates cherry production in Germany for MY5 2024/25 at 41,085 MT6. If realized, this would represent a 2.3% increase compared to the very low production of the previous year, but 13% below the ten-year average (2014-2023).

This is largely due to unfavorable climatic conditions during pollination. Late spring frosts reduced production, especially in the eastern part. Additionally, in the North, cold and wet weather reduced bee activity during the pollination of late varieties.

However, the actual harvested production may be significantly lower due to summer thunderstorms with heavy rain and hailstorms. As of mid-July 2024, it is unclear to what extent the recent storms with hail and heavy rain have affected production.

Sweet cherry production is estimated at 33,764 MT and sour cherry production at 7,321 MT. In MY 2023/24, production was 40,156 MT, of which 32,350 MT were sweet cherries and 7,806 MT were sour cherries. Depending on the region, harvesting started in the weeks between May 27 and June 3. In the North, this was about ten days earlier than the average, while in the South, it was slightly delayed. The harvest is expected to end in mid-August.

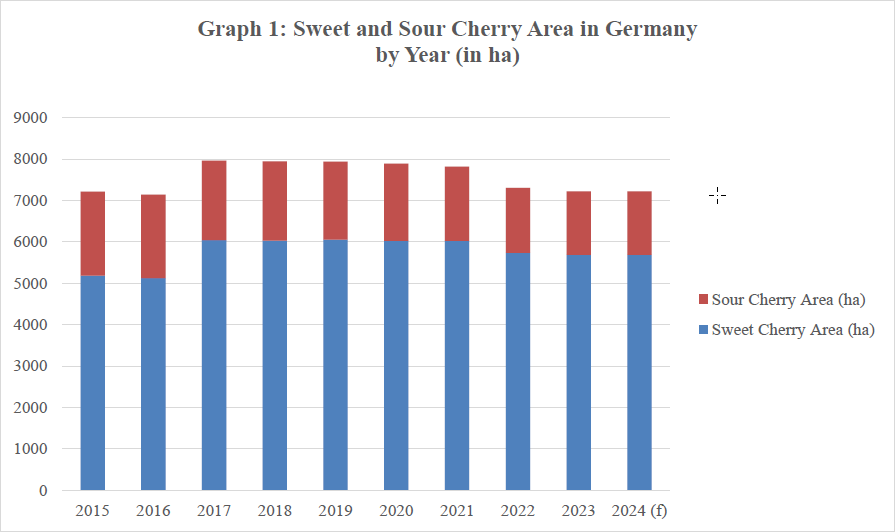

Image 1: Area planted (in hectares) with sweet and sour cherries in Germany by year.

Image 1: Area planted (in hectares) with sweet and sour cherries in Germany by year.

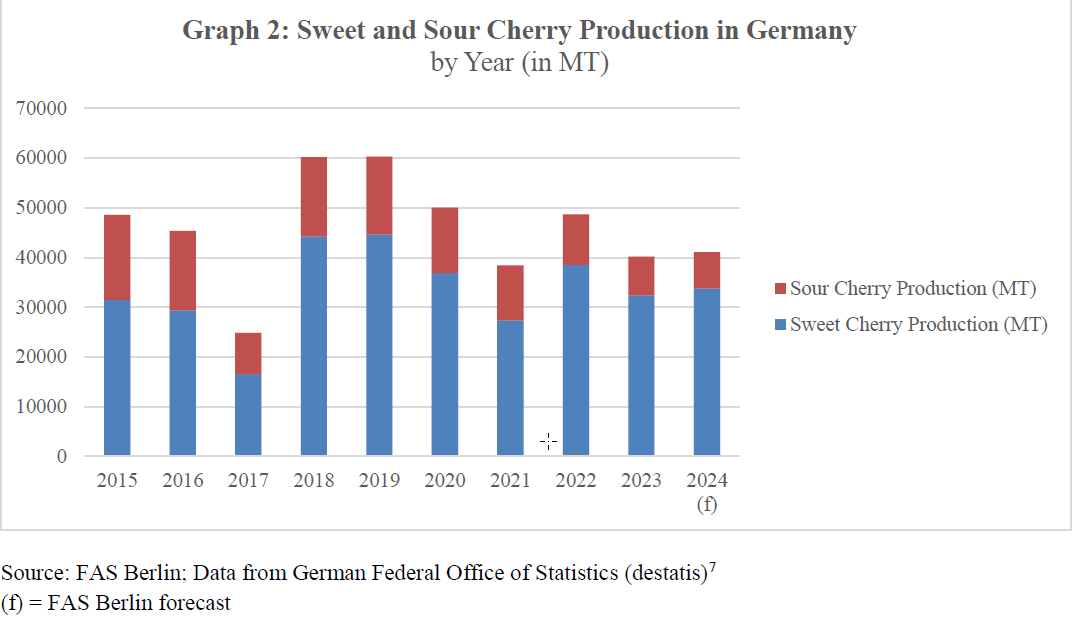

Image 2: Production (in tons) of sweet and sour cherries in Germany by year.

Image 2: Production (in tons) of sweet and sour cherries in Germany by year.

III. Trade

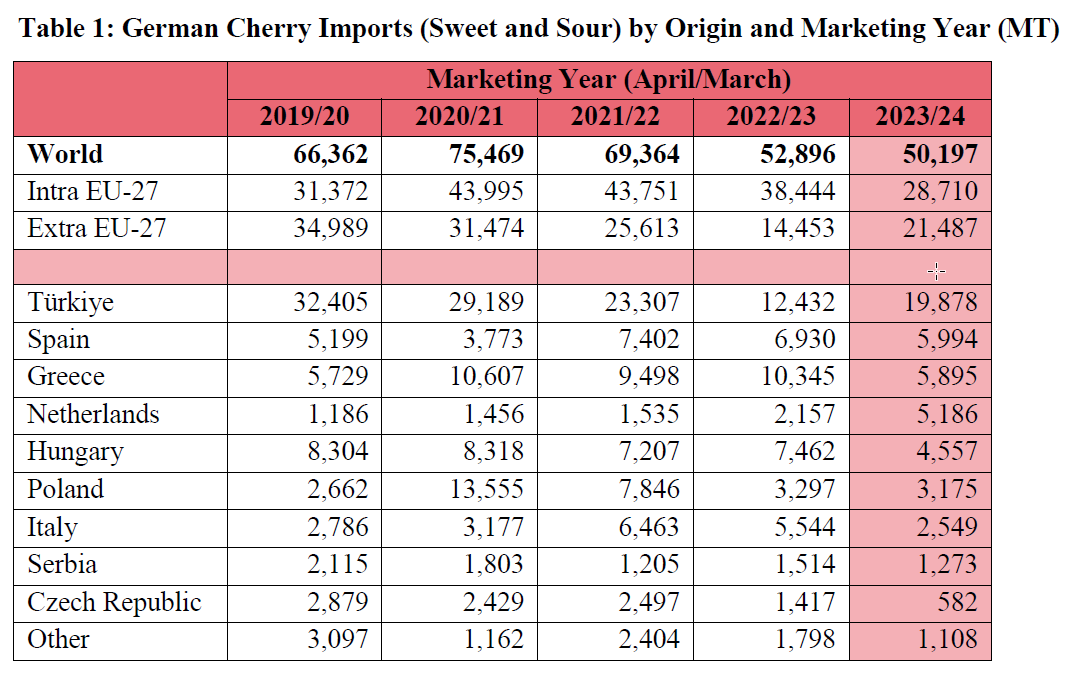

Germany is the third-largest cherry importer in the world, after China/Hong Kong and Russia. From 2010 to 2023, between 52% and 77% of the cherries consumed in Germany were imported, with imports ranging between 47,000 and 75,000 MT of cherries per year. Most of these were sweet cherries, accounting for between 60% and 81% depending on the year. Table 1: Imports (in tons) of cherries in Germany by origin and year.

Table 1: Imports (in tons) of cherries in Germany by origin and year.

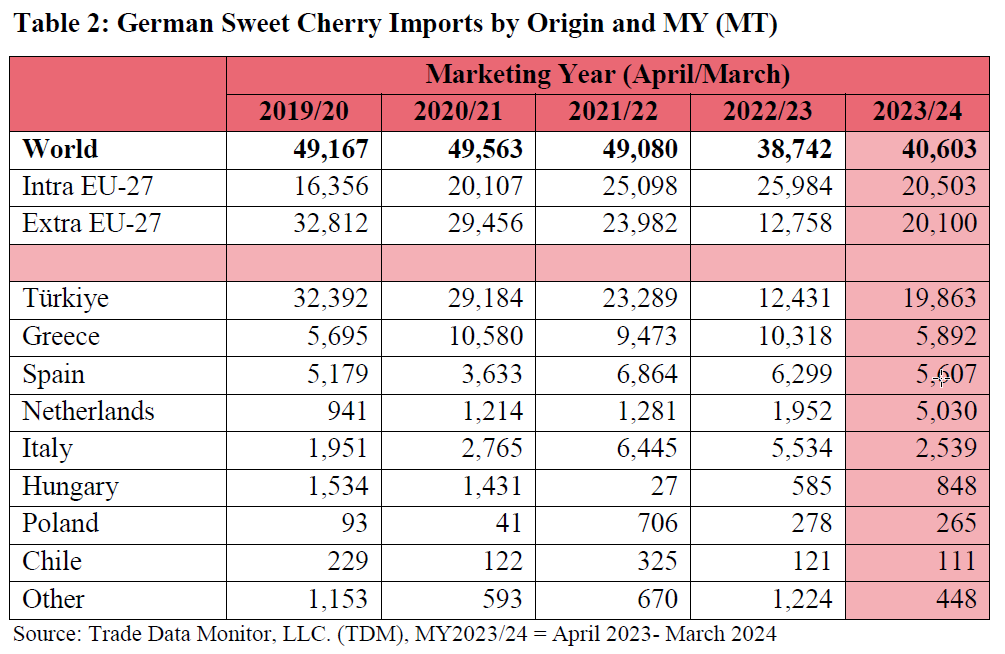

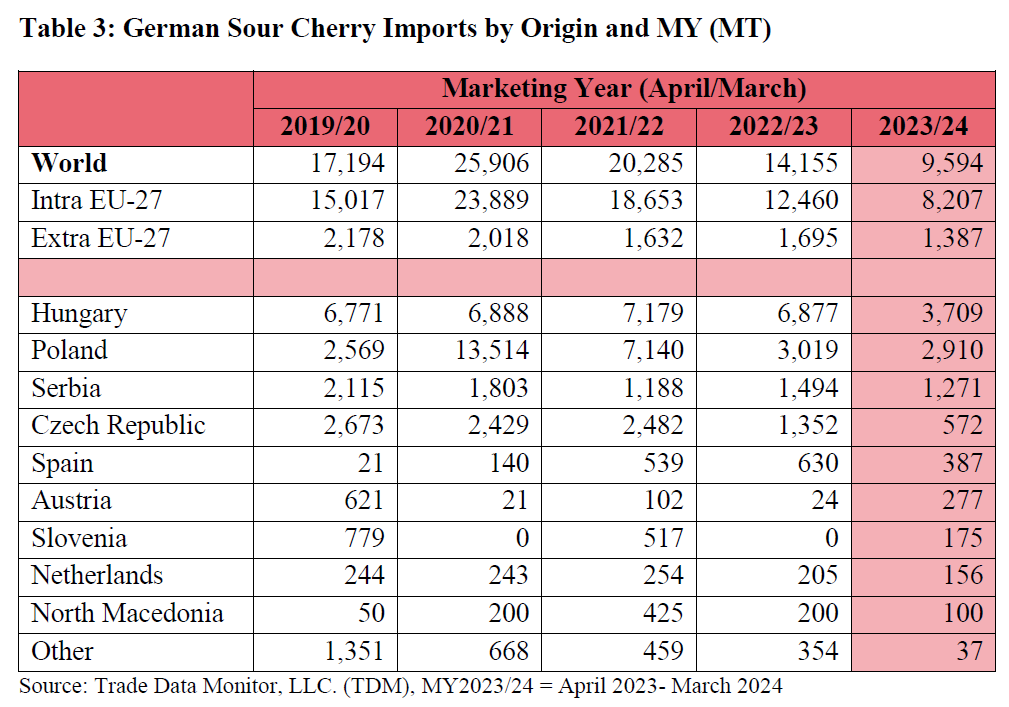

Turkey is by far the largest supplier, with a 40% share of the total import market and 49% if only sweet cherries are considered. Hungary, Poland, and Serbia are the major suppliers of sour cherries.

Table 2: Imports (in tons) of sweet cherries in Germany by origin and year.

Table 2: Imports (in tons) of sweet cherries in Germany by origin and year.

Imports from the United States are minimal. Opportunities for U.S. sweet cherries are better at both ends of the German domestic production cycle, i.e., late May/early June and August/September. Between the two periods, the latter is more promising as there is less competition from cheaper Turkish cherries.

Table 3: Imports (in tons) of sour cherries in Germany by origin and year.

Table 3: Imports (in tons) of sour cherries in Germany by origin and year.

In recent years, U.S. cherry exports to Germany have mainly occurred through other EU member states, especially the Netherlands. Direct imports from the United States are rare, with the last occurrence in MY 2018/19.

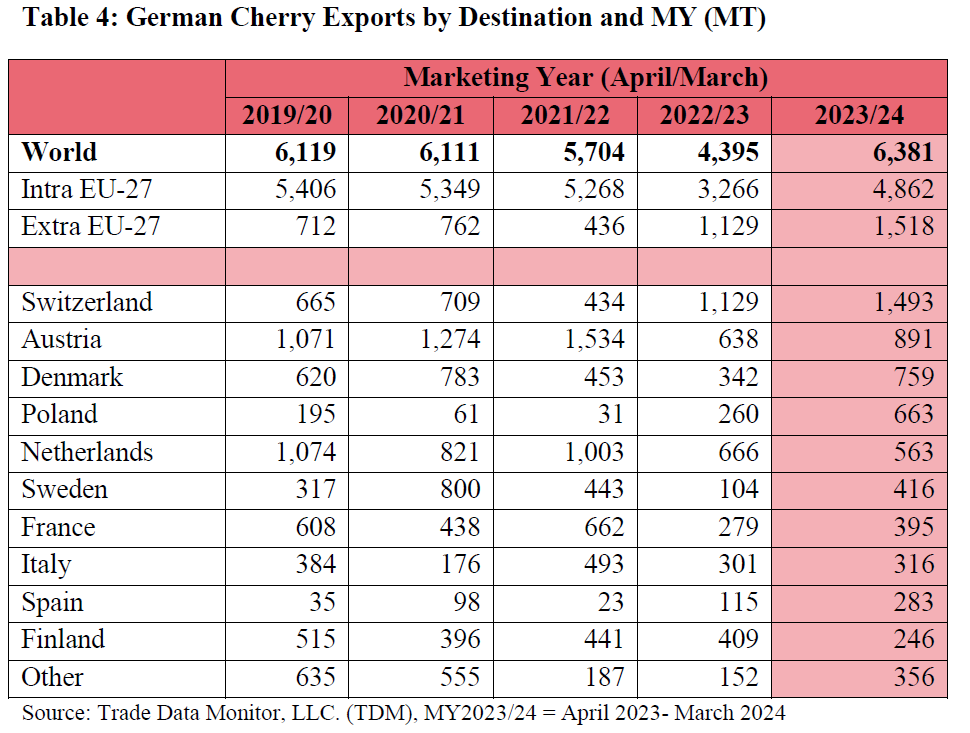

Germany exports less than 10% of its total cherry supply, between 4,000 and 6,400 tons in recent years. The main destinations are other EU member states such as the Netherlands, Austria, Denmark, and Sweden. The largest and almost exclusive non-EU destination for German cherries is Switzerland.

Table 4: Exports (in tons) of cherries from Germany by destination and year.

Table 4: Exports (in tons) of cherries from Germany by destination and year.

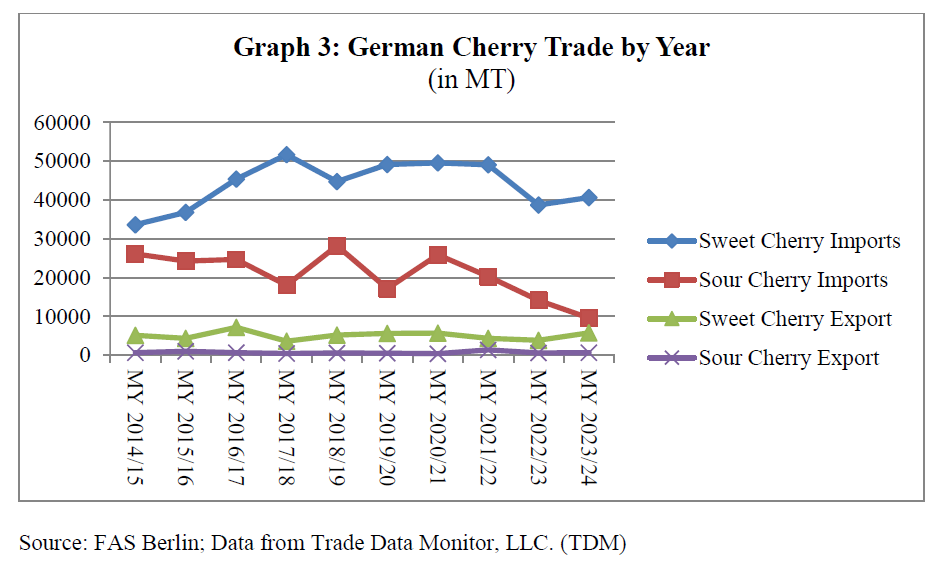

Image 3: Cherry trade in Germany (in tons) by year.

Image 3: Cherry trade in Germany (in tons) by year.

IV. Consumption

In Germany, fresh cherries are considered a seasonal product and are available in supermarkets mainly during the German marketing season (June/July). According to the German market information company Agrarmarkt Informations-Gesellschaft mbH (AMI) in 2022, 92.5% of households' purchases of sweet cherries occurred in June and July, and 5.2% in August8.

In contrast, peach purchases, which are rarely grown in Germany, are distributed more evenly between May and October. This seasonal availability explains the lower per capita consumption of cherries (2.2 kg) compared to peaches (2.8 kg). However, per capita consumption of cherries is more than double that of plums (1.0 kg).

In recent years, sweet cherries have become a trendy product that has benefited from increased health awareness and the growing popularity of snacks. Plums, on the other hand, are mainly used for baking and cooking.

Regarding sweet cherries, consumer preferences clearly lean towards larger sizes (>26 mm/1.024 inches). Smaller cherries are sold at a significant discount. For example, in the week of July 1, 2024, the average wholesale price of domestic sweet cherries was 5.92 euros ($6.23) per kg for the larger cherries but only 4.23 euros ($4.59) per kg for cherries smaller than 26 mm.

The demand for fresh sour cherries is steadily declining as the popularity of traditional cherry tart wanes. In MY23/24, 89% of nationally produced sour cherries were used for processing, mainly for canning or freezing (over 70%), while the remainder was used for juice production.

The percentage of sweet cherries used for processing ranges between 30% and 50%, depending on weather conditions during harvest, as rain damage increases the percentage allocated to canning or distillation into alcoholic beverages.

Processing cherries into dried fruit is uncommon in Germany. The low demand for dried cherries is met through imports. Due to the lack of a specific HS code for the product, there are no available data on trade in dried cherries.

Source: USDA

Images: USDA

Cherry Times - All rights reserved