The cherry continues to be the most relevant crop in the Chilean fruit industry.

However, its rapid growth, which has lasted for more than a decade, has brought the industry to a point where success no longer depends solely on producing and exporting more, but on how, when and under what conditions the fruit is placed on the market.

The 2025/26 season for Chilean cherries will be remembered as another campaign marking a before and after.

Signals from the season

Not necessarily because of a sudden collapse or a single event, but because it consolidated a series of signals that the industry had already been observing for several seasons: an increasingly demanding market, less tolerant of mistakes and much more sensitive to imbalances between supply, timing and quality.

The cherry continues to be the most relevant crop in the Chilean fruit industry in terms of value and exported volume, as well as cultivated area.

However, its rapid growth over more than a decade has brought the industry to a point where success no longer depends solely on producing and exporting more, but on how, when and under what conditions the fruit is placed on the market.

A market that has stopped responding automatically to volume

One of the most revealing elements of the season was the break in a pattern that had remained unchanged for years. In previous campaigns, a decline in prices associated with a sharp increase in the volume of cherries exported to China was usually followed by a price recovery in the following season.

This happened in 2015/16, 2018/19 and 2021/22 (see figure 1), all seasons following campaigns that had recorded increases of more than 50% year on year in exported volume (2014/15 +75%, 2017/18 +107% and 2020/21 +55%) and had shown a recovery in the average export FOB value.

In 2025/26, despite a significant decrease in shipments to China (-13%), following a campaign of historic volume with a 51% year-on-year increase, the expected recovery in the average price did not materialize.

Average prices

Official data as of February show that the campaign closed with an export unit value unchanged from the 2024/25 season, at USD 4.57 FOB/kg (approximately EUR 3.93 FOB/kg), 0.7% higher than the average value reported in 2024/25, which had been the lowest since the 2002/03 campaign.

This suggests that the market has reached a point of saturation where volume adjustments alone are no longer sufficient to support historically high price levels.

At the same time, the industry appears to have crossed a threshold in the balance between demand and supply in its main destination, forcing a review of assumptions that until recently had been taken for granted.

Beyond the specific data of a single season, the underlying message is that the accumulated growth of Chilean supply has begun to put pressure on the market’s absorption capacity.

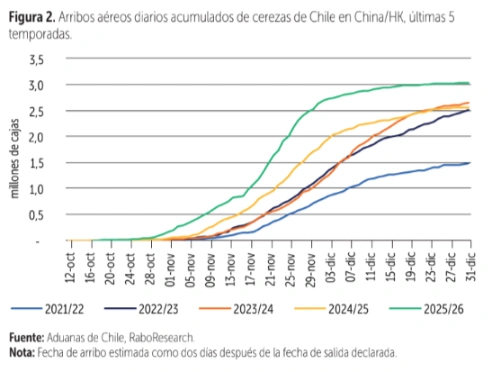

The timing factor: an exceptionally early season

While volume was a relevant component, the timing of the season proved decisive. The 2025/26 campaign was marked by a significant advance in harvests, exports and arrivals at destination, creating a dynamic never seen before in the industry.

A significant share of the total volume arrived on the Chinese market well ahead of Chinese New Year (see figure 2), the main commercial moment of the season.

It should be noted that at the end of the previous decade and in the early campaigns of this decade, it was normal to observe an increase in the average price in wholesale markets between two and three weeks before the date of Chinese New Year.

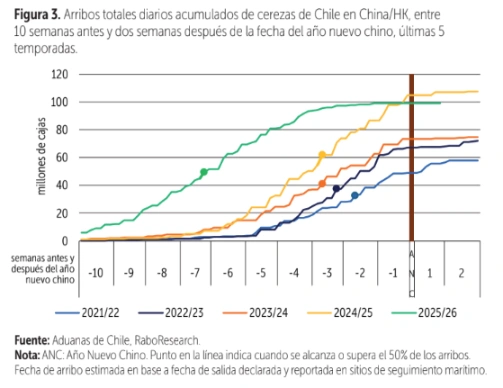

During the same period, in the 2021/22, 2022/23 and 2023/24 seasons, the industry managed to reach 50% of the total volume arriving during the season, with a quantity of around 37 million boxes.

Early arrivals

In the historic 2024/25 campaign, the market had 50% of the volume available three weeks before the date of Chinese New Year, with a quantity of 60 million boxes.

In the 2025/26 campaign, 50% of arrivals occurred seven weeks earlier, while in the period between two and three weeks before the holiday, the volume of arrivals exceeded everything previously observed, with 98 million boxes, practically the entire volume (see figure 3).

This advance changed the usual market sequence, reducing the space in which expectation and upward pressure on prices had historically been generated.

The early and abundant availability of cherries in the 2025/26 campaign may have changed the consumer’s perception of the product.

When the fruit is massively available for several weeks before the key period, it loses part of its exceptional and exclusive character and becomes more quickly integrated into the regular fresh fruit retail offer. In this context, willingness to pay becomes more sensitive to price and less dependent on symbolism or seasonality.

Commercial pressure in a system that allows no mistakes

The marketing campaign for Chilean cherries in China has a relatively narrow commercial window, and the product has a shorter shelf life than other fruits.

This means that the pressure to sell is high and that, with each new season, the margins for error become increasingly narrow.

In a scenario of high and concentrated arrivals, any deviation in terms of quality or condition quickly translates into discounts that end up affecting the entire market. The 2025/26 campaign was no exception.

From the first weeks of the season, recurring comments came from the Chinese market about fruit with low firmness and sizes below expectations.

Required quality

In a highly competitive market, these factors carried greater weight than in previous seasons. The presence of fruit with quality and/or condition problems does not affect only the lots involved, but also tends to drag down the prices of the rest of the supply, even fruit that meets the expected standards.

The 2025/26 experience reinforces a concept that had already emerged in previous campaigns: quality has stopped being a differentiating attribute and has become a basic requirement for being present on the market.

In a context of high supply and competition, consistency in terms of firmness, size and condition becomes a determining factor in sustaining returns.

China: from premium market to more rational market

Another of the structural changes consolidated during the season concerns the evolution of the Chinese consumer.

For several years, the cherry was successfully positioned as a gift product, associated with the celebration of Chinese New Year, status, scarcity and high value.

However, greater availability, repeat purchasing and the normalization of consumption are moving the market towards a more rational and less emotional logic.

This does not directly imply a decrease in the importance of China as a destination, but rather a transformation in the way demand behaves and in how this change will need to be addressed in the future. The Chinese consumer is exposed to the product earlier and earlier, compares prices and adjusts purchasing decisions according to perceived value.

Unit values

In this scenario, the level and timing of early supply could tend to weaken the bargaining power on prices of mid- and late-season supply.

Even more so considering that in the previous campaign, 2024/25, Chinese consumers had been exposed to record levels of supply and had their first encounter with cherries at prices significantly lower than in previous campaigns.

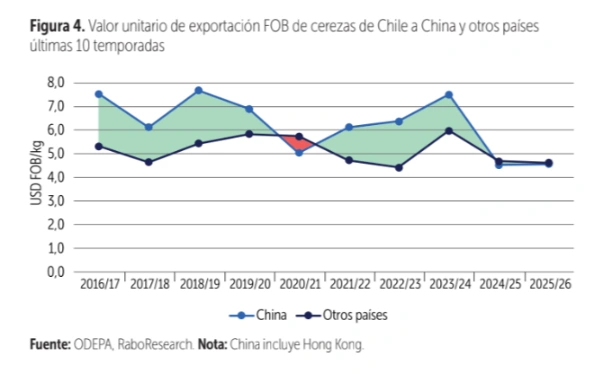

A further element that deserves attention is the convergence observed in export unit values between China and other destinations.

For years, the Chinese market offered a clear premium compared with the rest of the world: USD 1.5 FOB/kg (approximately EUR 1.29 FOB/kg), or 29% more on average between 2014/15 and 2023/24.

In the last two seasons, this difference has disappeared: the average export unit value to “other destinations outside China”, taken as a whole, was slightly higher (+USD 0.1/kg) (+EUR 0.09/kg) than the export value to China and Hong Kong (see figure 4).

In the future, this could change the traditional incentives for allocating volumes mainly to China, since today there are destinations with export unit values that are higher, similar or even lower than China’s, but which may offer advantages in transport costs or receive a larger share of non-premium supply, among other factors capable of ensuring competitive profitability.

Diversification: an opportunity that requires precision

Diversification of markets has been a recurring objective for the industry, but the results of the 2025/26 season have given it a new sense of urgency.

Although shipments to destinations other than China reached record volumes, their share of the total remains limited (13%) and concentration on China continues to be high.

This is a factor that will continue to be debated in the coming seasons, if volume continues to grow as expected.

The challenge is not only to open new markets, but to do so in an orderly way. Many of these destinations have significantly smaller populations and seasonal cherry consumption concentrated in the northern hemisphere summer; as a result, they have a more limited absorption capacity during the counter-season.

Emerging markets

Flooding these emerging markets with fruit, even of good quality, without adequate preparation could replicate the same problems observed in China.

In this context, destinations such as the United States have shown interesting signals. Their growth has been gradual and, so far, has not generated severe pressure on prices, despite a record figure of arrivals being recorded (5.1 million boxes).

This suggests that there is room to continue developing the market, provided a prudent and well-calibrated strategy is maintained.

In addition, its consumption calendar offers opportunities to position the Chilean cherry around different holidays and times of the year, reducing dependence on a single commercial event.

Export figures show several destinations, after China and the United States, in Europe, Asia and Latin America, each with different realities and opportunities to study in view of a more complex scenario in the coming seasons.

Looking ahead: adjustments rather than breaks

The 2025/26 season does not represent a definitive break for the industry, but certainly a warning.

The growth of cherry production in Chile will continue in the coming years, driven by new orchards entering full production and by improvements in productivity.

In this scenario, pressure on the system will be permanent. The main challenge will be to move from a model based on volume to one based on efficiency, planning, diversification and consistency.

New phase

This implies more selective decisions in the field, in processing and in packaging, as well as a more accurate reading of the export calendar, more coordinated logistics management and a commercial strategy that takes into account the real capacity of each market.

The Chilean cherry maintains solid foundations and a privileged position at global level.

However, the competitive context has changed. The industry now faces a scenario in which its main destination market is no longer the same as it was ten or even five seasons ago.

A market in which consumers now know what it means to pay less for a product that less than ten years ago they perceived as a luxury, and that today no longer forgives imbalances in terms of quality and condition.

A market in which, moreover, profitability will depend on the ability to adapt to this new phase of maturity, in a global context once again entering a period of uncertainty.

```

Gonzalo Salinas, senior food and agribusiness research analyst at Rabobank

```

Text and figure source: Redagricola

Opening image source: Stefano Lugli

Cherry Times - All rights reserved