In the Pacific Northwest, the cherry harvest is now in full swing, but early market signals do not appear to be delivering the turnaround growers had been hoping for. After several seasons marked by difficult prices, in some cases even below harvesting costs, many operators had viewed 2026 as the year of a possible recovery.

According to Tim Delbridge, an economist at Oregon State University, expectations for prices are proving more cautious than anticipated. The values emerging from early data and market indications do not seem to be reaching the levels cherry growers had hoped for.

Flat prices and still-high costs

The main issue remains the combination of insufficient returns and production costs that are still high. Delbridge notes that the prices paid to growers have not shown any significant improvement, while the expenses required to maintain production continue to weigh on farm budgets.

The economic pressure is already visible in some growing areas: outside The Dalles, some acreage has been left unmanaged, a concrete sign of the financial difficulties affecting some farms.

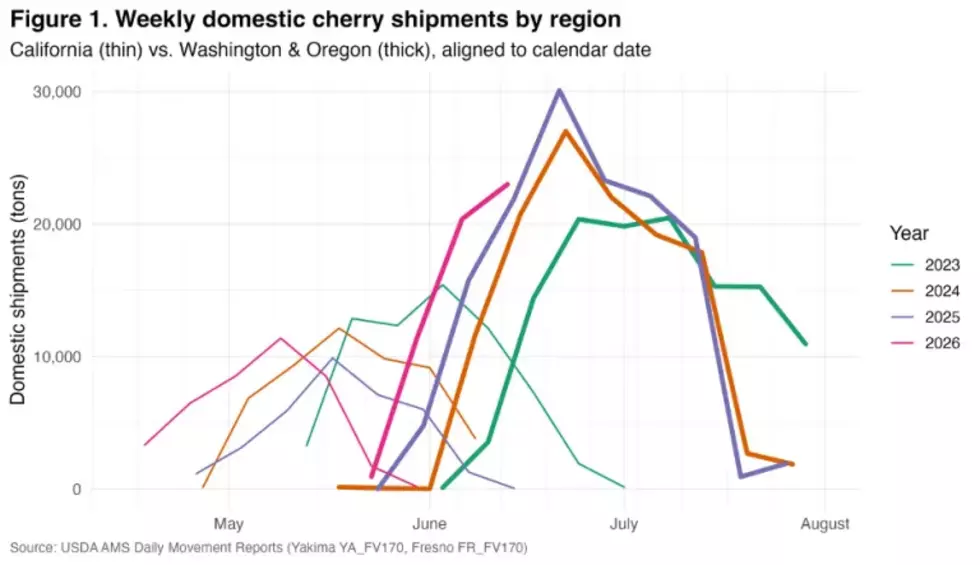

An early harvest complicating the market

The production calendar is also making the situation more delicate. The harvest is running about two weeks earlier than normal, a factor that may have created some friction in retailer planning.

Despite the complex context, Delbridge remains cautiously optimistic. Demand linked to the month of July, the period following the July 4th holiday and the final phase of the season could still support prices.

With the peak in volumes now behind us, any higher prices in the closing part of the campaign could help recover at least part of the season’s profitability.

The gap between shelf and field is widening

One of the most significant aspects highlighted by the economist concerns the growing gap between the price paid by consumers and the price received by growers. In June, advertised retail prices were more than 2 dollars per pound higher, approximately €1.84 per 0.45 kg, than shipping point prices, one of the widest spreads recorded in the past five years.

For growers, this gap reinforces the feeling of imbalance along the supply chain: while consumers continue to see strong prices on supermarket shelves, the value returning to the source does not appear sufficient to offset costs and production risks.

Difficult decisions on the horizon

After several consecutive years of problematic prices, Delbridge stresses that the sector may be facing increasingly difficult choices. The combination of weak prices, high costs and reduced margins risks accelerating structural decisions regarding orchard management, investments and production continuity.

Final data on yields and economic returns for growers will only be available in several months. However, the initial picture suggests that the strong season many cherry growers needed to rebuild profitability has not yet materialized.

Text and chart source: pnwag.net

Opening image source: Stefano Lugli

Cherry Times - All rights reserved