The 2025-2026 season marked a turning point for the industry: the market began to push out less competitive producers and severely penalize lower-quality cherries.

The Chilean cherry industry is going through one of the most complex and decisive periods in its recent history.

Far from the euphoria that characterized the sector over the past decade, the 2025-2026 season confirmed a structural shift in the business: lower volumes no longer guarantee better prices, and profitability is no longer assured simply by exporting.

This is what emerges from an in-depth report prepared by Francisco Duboy and Sebastián Cartwright, from the consulting firm CyD Agromanagement, which analyzes the industry’s performance using an evocative economic metaphor: the “invisible hand” theorized by Adam Smith.

The failure of self-regulation

According to the report, faced with the sector’s inability to regulate itself, the market itself began to organize the activity, rewarding quality and harshly penalizing less competitive producers.

Chile has established itself as the world’s leading exporter of cherries from the Southern Hemisphere. However, despite the high level of professionalization and access to market information that characterize the industry, the sector has failed to establish effective self-regulation mechanisms.

During the 2025-2026 campaign, the attempt promoted by the Sociedad Nacional de Agricultura (SNA), Frutas de Chile and Fedefruta to set mandatory minimum quality and size standards for exported fruit failed once again.

The absence of agreements among industry organizations left the market as the only arbiter. And the verdict was clear: settlements are heavily penalizing lower-quality fruit, generating a real selection process within the sector.

“The market is doing the work that the industry failed to achieve at an institutional level,” argue the authors of the study, warning that remaining in the business will increasingly depend on the ability to produce excellent fruit.

Less fruit, but no price recovery

One of the most significant findings of the report is that the expected recovery in prices never materialized, despite the reduction in exported volumes.

The research analyzed a sample of more than 33 million kilos, from 31 exporters and 33 varieties, representative of around 5% of the cherry-growing area in Chile, equal to approximately 3,300 hectares.

The results show that the season closed with around 112 million boxes exported, a figure significantly lower than the historical record of 125.2 million reached the previous year. However, this reduction of about 9% was not enough to reverse the decline in prices.

The explanation seems to lie in the enormous dependence on the Chinese market, a destination that absorbed 87% of Chilean shipments. According to the study, once the threshold of 100 million exported boxes is exceeded, the market stops reacting in a stable way and enters a saturation zone, where prices remain depressed.

The confirmation of low prices

The 2024-2025 campaign had already shown worrying signs. Despite the record volume of 626,014 tons exported, the average FOB price fell by 29% per kilo.

The most concerning aspect is that during the 2025-2026 season, the industry failed to recover value, ending up consolidating around this new level of low prices.

The deterioration of returns

The analysis of the Weighted Net Return (WNR) by shipment week confirms the deterioration of profitability. The return curve for the 2025-2026 campaign was systematically below that of the previous season during the second half of the export period.

One of the most relevant developments was the rapid downward break through the US$4 threshold (around €3.51) per kilo. According to the report, this occurred around week 48, much earlier than expected, and from that point onward prices continued to fall without showing signs of recovery.

The distribution of shipments is also a cause for concern. Almost half of the exported fruit, equal to 47% of the total, was marketed during weeks in which the average return was below US$2 (around €1.75) per kilo.

At the opposite end, only 9% of production managed to obtain returns equal to or above US$4 (around €3.51) per kilo. According to the specialists, this situation highlights a growing concentration of fruit in the so-called “negative range” of prices, significantly reducing the possibility of achieving attractive margins.

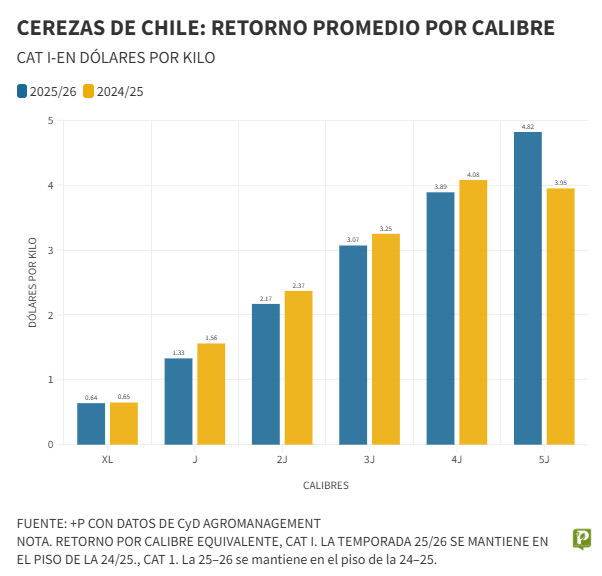

Fruit size becomes the key to the business

If there is one clear conclusion in the report, it is the enormous importance acquired by fruit size.

The difference between producing small or large cherries is no longer simply a commercial improvement: today it can mean survival or exit from the market. The data is eloquent.

While an XL size grade barely exceeds US$0.6 (around €0.53) per kilo, a 4J size grade reaches returns close to US$3.9 (around €3.42) per kilo, almost six times more.

As a result, producing L and XL size grades under current conditions appears to be a financially unsustainable strategy.

The price gap

“The price gap between large and small fruit is the main tool through which the invisible hand is cleansing the market,” state Duboy and Cartwright.

This phenomenon is forcing producers to rethink their agronomic strategies, prioritizing crop load, pruning, nutrition and production regulation, with the aim of maximizing fruit size.

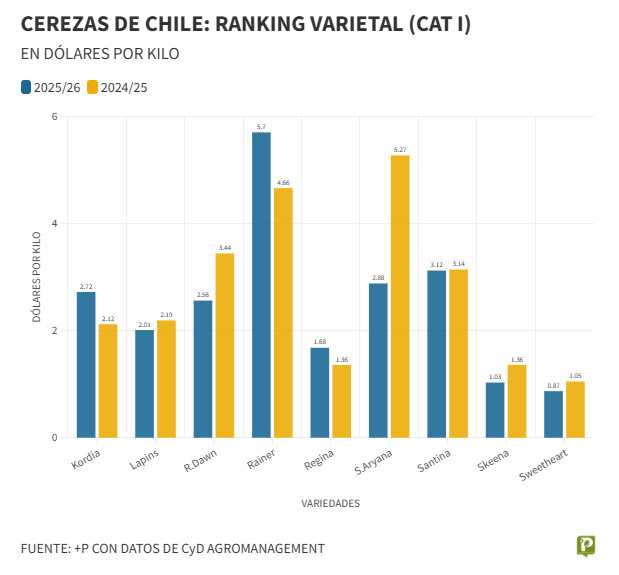

Santina continues to lead among traditional varieties

The study also analyzed the performance of the main varieties grown in Chile. Three varieties continue to largely dominate the supply intended for export: Lapins, Santina and Regina, which together account for more than 80% of national shipments.

Santina once again ranked as the best-performing variety among those with the highest volumes, recording a Weighted Net Return of US$3.12 (around €2.74) per kilo. Its advantage mainly derives from its nature as an early variety, which allows it to access more favorable commercial windows.

Lapins, the most widely grown variety in the country, showed a downward trend and reached only US$2.01 (around €1.76) per kilo, reflecting the difficulties faced by supply concentrated during periods of greater competition.

Regina, for its part, recorded a slight recovery compared with the previous campaign, reaching US$1.68 (around €1.47) per kilo. However, the report warns that the variety still shows no clear signs of recovery.

Among the varieties with a smaller market share, Rainier stood out for its high average returns, close to US$5.70 (around €5.00) per kilo. By contrast, Sweet Aryana suffered a sharp decline, falling from US$5.27 (around €4.62) to just US$2.88 (around €2.53).

The authors emphasize that new genetics do not automatically guarantee better commercial results. Success will depend on the ability of the variety to adapt correctly to the harvest window and meet the quality standards required by the market.

A turning point for the industry

The conclusions of the report are clear and represent a warning for the entire sector.

The industry cannot expect the market to spontaneously save producers through price increases. On the contrary, the steady growth of the cultivated area suggests that pressure on supply will continue in the coming years.

In this context, survival will depend on three key factors: rigorous control of costs, elimination of inefficiencies and production of high-quality fruit.

The study recommends keeping production costs below US$2 (around €1.75) per kilo and, ideally, bringing them closer to US$1.5 (around €1.32) per kilo.

Difficult decisions

At the same time, it highlights the need to make difficult decisions, such as converting varieties that have lost competitiveness or even removing low-productivity orchards.

The 2025-2026 season, the specialists conclude, marks a before and after for the Chilean cherry business. Profitability is no longer guaranteed simply by belonging to a successful export industry.

From now on, only those able to achieve operational excellence, high quality standards and efficient commercial management will be able to remain competitive in an increasingly demanding global market.

Text and chart source: Mas Produccion, CyD Agromanagement, Smartcherry and editorial contributions +P

Opening image source: Stefano Lugli

Cherry Times - All rights reserved